Contents

Overview

The concept of manipulating interest rates to influence economic activity has roots stretching back to the early days of central banking. While formal, systematic rate adjustments are a 20th-century phenomenon, precursors can be seen in the actions of institutions like the Bank of England in the 19th century, which would adjust its 'Bank Rate' to manage gold reserves and credit conditions. The modern era of deliberate interest rate policy truly took shape after the Great Depression, with institutions like the Federal Reserve in the United States increasingly using the federal funds rate as a primary tool. The Kennedy administration saw significant use of monetary policy to manage growth, and post-war economic management by central bankers like Paul Volcker (though known for hikes) underscored the power of rate adjustments. The establishment of independent central banks, such as the European Central Bank, further solidified the global practice of using rate cuts and hikes as a key lever for economic stability.

⚙️ How It Works

Interest rate cuts function by lowering the cost of money. When a central bank, like the Federal Reserve, cuts its target for the federal funds rate—the rate at which commercial banks lend reserves to each other overnight—it reduces the borrowing costs for these banks. This reduction typically prompts commercial banks to lower their own prime lending rates, which are the benchmark rates for many consumer and business loans. Consequently, individuals and corporations find it cheaper to take out mortgages, car loans, business expansion loans, and other forms of credit. This increased availability of cheaper credit is intended to stimulate consumer spending and business investment, thereby boosting aggregate demand and encouraging economic growth. The mechanism is designed to combat deflationary pressures and sluggish economic activity by making borrowing and spending more attractive than saving.

📊 Key Facts & Numbers

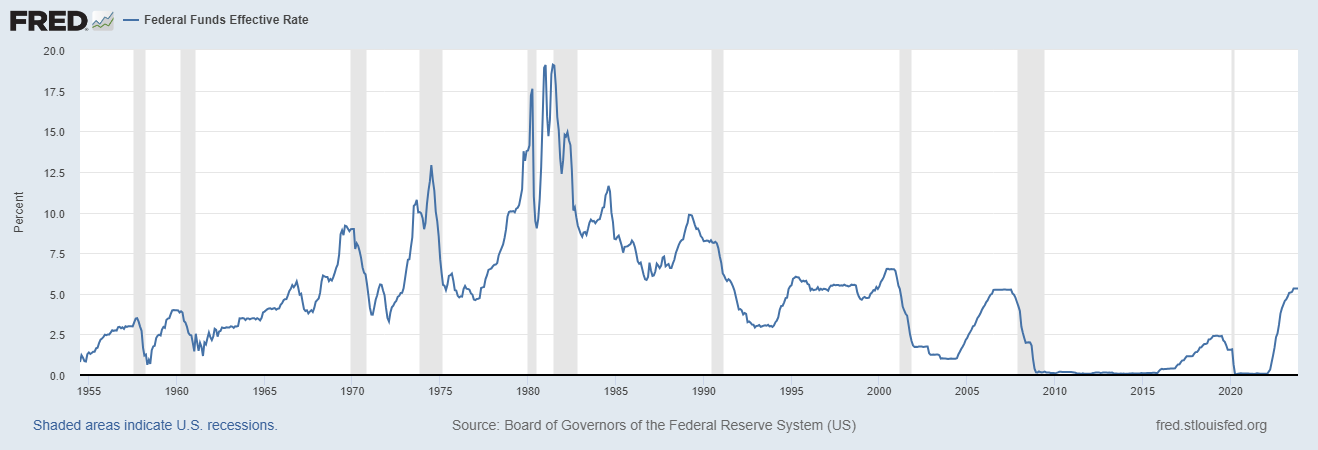

Central banks have historically made significant rate cuts during economic downturns. Following the 2008 financial crisis, the Federal Reserve slashed its benchmark rate from 5.25% in September 2007 to a range of 0-0.25% by December 2008. The federal funds rate was maintained at a near-zero level for seven years after December 2008. Similarly, the Bank of Japan has experimented with negative interest rates, pushing its policy rate below zero in an attempt to stimulate its long-stagnant economy. In the wake of the COVID-19 pandemic, the Fed again cut rates, bringing them down to the 0-0.25% range. The average cut size globally in 2020 was approximately 0.50 percentage points, with some economies experiencing cuts of 1.00 percentage point or more.

👥 Key People & Organizations

Key figures and organizations orchestrate interest rate decisions. The Federal Reserve, led by Chair Jerome Powell, is paramount in the United States, with its Federal Open Market Committee (FOMC) making the final calls. Globally, institutions like the European Central Bank (ECB), headed by Christine Lagarde, and the Bank of Japan (BoJ), under Governor Kazuo Ueda, play similar roles. Economists and financial analysts at institutions like Goldman Sachs and J.P. Morgan closely monitor and forecast these decisions. International bodies such as the International Monetary Fund (IMF) often provide guidance and analysis on the effectiveness of rate policies across member nations, influencing global monetary policy discussions.

🌍 Cultural Impact & Influence

Interest rate cuts have profound cultural and societal implications, shaping everything from household budgets to global investment flows. The accessibility of cheaper mortgages, facilitated by rate cuts, has historically fueled housing booms and influenced suburban development patterns in countries like the United States. For individuals, lower rates can translate into more affordable student loans and car payments, impacting disposable income and consumer confidence. On a broader scale, prolonged periods of low interest rates, often a consequence of aggressive rate cuts, can lead to asset price inflation, creating wealth for those invested in stocks and real estate, while potentially widening the wealth gap for those without such assets. The pursuit of yield in a low-rate environment has also driven innovation in financial products and encouraged greater risk-taking among investors, influencing the overall financial culture.

⚡ Current State & Latest Developments

The current landscape sees many central banks having recently completed a cycle of aggressive rate hikes to combat inflation. The focus has now shifted to when and how quickly these rates might be cut. The European Central Bank has signaled a potential start to cuts in mid-2024, while the Bank of England is also under pressure to ease policy as inflation subsides. The narrative is shifting from fighting inflation to managing a potential economic slowdown.

🤔 Controversies & Debates

The efficacy and consequences of interest rate cuts are subjects of intense debate. A primary controversy revolves around the potential for rate cuts to fuel asset bubbles and excessive risk-taking, as seen in discussions surrounding the 2008 financial crisis and subsequent periods of quantitative easing. Critics argue that prolonged low rates disproportionately benefit asset owners, exacerbating wealth inequality. Another debate centers on the 'zero lower bound' problem: when rates approach zero, central banks have less room to maneuver with traditional cuts, leading to the exploration of unconventional policies like negative interest rates or forward guidance, which themselves carry risks and uncertainties. Furthermore, the global spillover effects of one major central bank's rate cuts can destabilize other economies, particularly emerging markets, by influencing capital flows and currency values.

🔮 Future Outlook & Predictions

The future outlook for interest rate cuts is intrinsically tied to the trajectory of global inflation and economic growth. As inflation continues to moderate from its recent peaks, many economists anticipate a gradual easing of monetary policy across major economies in 2024 and 2025. The pace of these cuts will likely be cautious, with central banks aiming to avoid reigniting inflation while also preventing a severe recession. Some analysts predict a 'soft landing' scenario where rate cuts help stabilize growth without triggering a significant economic downturn. However, geopolitical risks, persistent supply chain issues, and unexpected inflationary shocks could alter this outlook, potentially delaying or even reversing planned cuts. The long-term trend might see central banks recalibrating their policy frameworks in light of lessons learned from recent inflationary episodes and the challenges of the zero lower bound.

💡 Practical Applications

Interest rate cuts have direct practical applications in various economic scenarios. For governments, cutting rates can make it cheaper to finance national debt, reducing the burden of interest payments. Businesses utilize lower rates to fund capital expenditures, research and development, and expansion projects, thereby fostering innovation and job creation. For individuals, rate cuts translate into more affordable homeownership through lower mo

Section 11

Interest rate cuts function by lowering the cost of money. When a central bank, like the Federal Reserve, cuts its target for the federal funds rate—the rate at which commercial banks lend reserves to each other overnight—it reduces the borrowing costs for these banks. This reduction typically prompts commercial banks to lower their own prime lending rates, which are the benchmark rates for many consumer and business loans. Consequently, individuals and corporations find it cheaper to take out mortgages, car loans, business expansion loans, and other forms of credit. This increased availability of cheaper credit is intended to stimulate consumer spending and business investment, thereby boosting aggregate demand and encouraging economic growth. The mechanism is designed to combat deflationary pressures and sluggish economic activity by making borrowing and spending more attractive than saving.

Section 12

Central banks have historically made significant rate cuts during economic downturns. Following the 2008 financial crisis, the Federal Reserve slashed its benchmark rate from 5.25% in September 2007 to a range of 0-0.25% by December 2008. The federal funds rate was maintained at a near-zero level for seven years after December 2008. Similarly, the Bank of Japan has experimented with negative interest rates, pushing its policy rate below zero in an attempt to stimulate its long-stagnant economy. In the wake of the COVID-19 pandemic, the Fed again cut rates, bringing them down to the 0-0.25% range. The average cut size globally in 2020 was approximately 0.50 percentage points, with some economies experiencing cuts of 1.00 percentage point or more.

Section 13

Key figures and organizations orchestrate interest rate decisions. The Federal Reserve, led by Chair Jerome Powell, is paramount in the United States, with its Federal Open Market Committee (FOMC) making the final calls. Globally, institutions like the European Central Bank (ECB), headed by Christine Lagarde, and the Bank of Japan (BoJ), under Governor Kazuo Ueda, play similar roles. Economists and financial analysts at institutions like Goldman Sachs and J.P. Morgan closely monitor and forecast these decisions. International bodies such as the International Monetary Fund (IMF) often provide guidance and analysis on the effectiveness of rate policies across member nations, influencing global monetary policy discussions.

Section 14

Interest rate cuts have profound cultural and societal implications, shaping everything from household budgets to global investment flows. The accessibility of cheaper mortgages, facilitated by rate cuts, has historically fueled housing booms and influenced suburban development patterns in countries like the United States. For individuals, lower rates can translate into more affordable student loans and car payments, impacting disposable income and consumer confidence. On a broader scale, prolonged periods of low interest rates, often a consequence of aggressive rate cuts, can lead to asset price inflation, creating wealth for those invested in stocks and real estate, while potentially widening the wealth gap for those without such assets. The pursuit of yield in a low-rate environment has also driven innovation in financial products and encouraged greater risk-taking among investors, influencing the overall financial culture.

Section 15

The current landscape sees many central banks having recently completed a cycle of aggressive rate hikes to combat inflation. The focus has now shifted to when and how quickly these rates might be cut. The European Central Bank has signaled a potential start to cuts in mid-2024, while the Bank of England is also under pressure to ease policy as inflation subsides. The narrative is shifting from fighting inflation to managing a potential economic slowdown.

Section 16

The efficacy and consequences of interest rate cuts are subjects of intense debate. A primary controversy revolves around the potential for rate cuts to fuel asset bubbles and excessive risk-taking, as seen in discussions surrounding the 2008 financial crisis and subsequent periods of quantitative easing. Critics argue that prolonged low rates disproportionately benefit asset owners, exacerbating wealth inequality. Another debate centers on the 'zero lower bound' problem: when rates approach zero, central banks have less room to maneuver with traditional cuts, leading to the exploration of unconventional policies like negative interest rates or forward guidance, which themselves carry risks and uncertainties. Furthermore, the global spillover effects of one major central bank's rate cuts can destabilize other economies, particularly emerging markets, by influencing capital flows and currency values.

Section 17

The future outlook for interest rate cuts is intrinsically tied to the trajectory of global inflation and economic growth. As inflation continues to moderate from its recent peaks, many economists anticipate a gradual easing of monetary policy across major economies in 2024 and 2025. The pace of these cuts will likely be cautious, with central banks aiming to avoid reigniting inflation while also preventing a severe recession. Some analysts predict a 'soft landing' scenario where rate cuts help stabilize growth without triggering a significant economic downturn. However, geopolitical risks, persistent supply chain issues, and unexpected inflationary shocks could alter this outlook, potentially delaying or even reversing planned cuts. The long-term trend might see central banks recalibrating their policy frameworks in light of lessons learned from recent inflationary episodes and the challenges of the zero lower bound.

Section 18

Interest rate cuts have direct practical applications in various economic scenarios. For governments, cutting rates can make it cheaper to finance national debt, reducing the burden of interest payments. Businesses utilize lower rates to fund capital expenditures, research and development, and expansion projects, thereby fostering innovation and job creation. For individuals, rate cuts translate into more affordable homeownership through lower mo

Key Facts

- Category

- economics

- Type

- topic